- EU gross box office dropped by 3.3% to a total of EUR 6.80 billion in 2018, the lowest level in four years

- Superhero blockbuster Avengers: Infinity Wars and family animation Incredibles 2 topped the EU charts

- Market share for European films rose to 29.4%

- EU film production continued to grow after a pause in 2017, to 1 847 films produced

- Digital screen penetration in the EU reached 97%

EU gross box office down by 3.3% in 2018

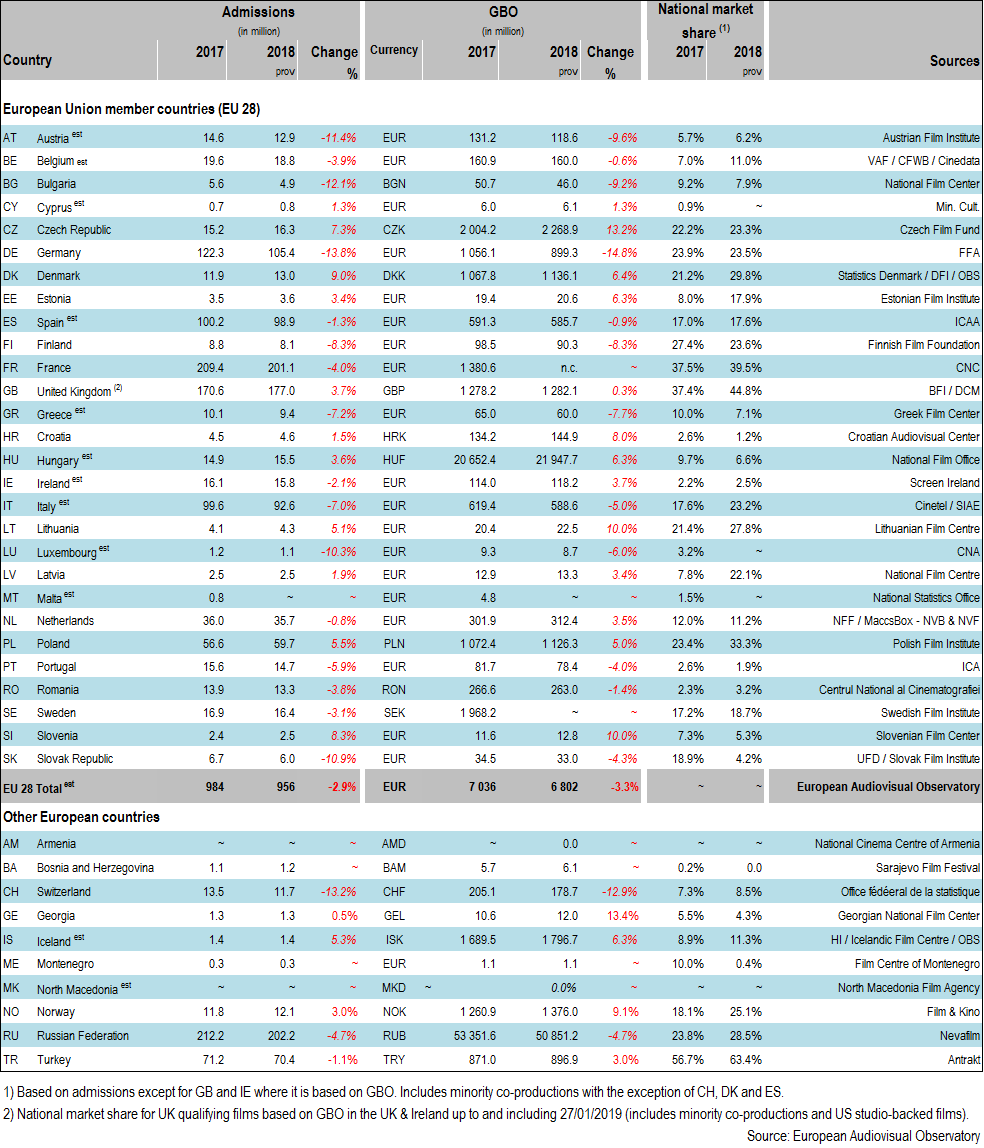

For the first time in four years, cumulative GBO in the EU Member States did not pass the EUR 7 billion benchmark in 2018. Based on provisional data, the European Audiovisual Observatory estimates that cumulative GBO takings in the EU fell by 3.3% in 2018 to a total of EUR 6.80 billion: EUR 233.3 million less than in 2017. Not adjusted for inflation, this represents the lowest result since 2014; however, it remains the fourth highest level in the last decade. With the pan-European average ticket price stable at EUR 7.1, the downturn in revenues reflects a drop in the number of tickets sold, as EU cinema attendance fell by 2.9% to 956 million tickets sold, 28.7 million less than in 2017. As in previous years GBO revenues evolved unevenly across the EU, increasing in 12 and decreasing in 11 EU territories, while remaining relatively stable in 3 of the 26 EU markets for which provisional data were available. The decrease in box office receipts was primarily driven by a sizeable dip registered in Germany (-EUR 156.8 million, -14.8%). Among the other four major EU markets, GBO also declined in Italy (-EUR 30.8 million, -5.0%) and France while remaining comparatively stable in Spain (-EUR 5.6 million, -0.9%) and the United Kingdom (+GBP 3.9 million, +0.3%). Conversely, GBO grew in several Central and Eastern European markets, with an upturn in Czech Republic (+13.2%), Lithuania (+10.0%), SIovenia (+10.0%), Croatia (+8.0%), Hungary (+6.3%), and Poland (+5.0%).

Outside the EU, Russian GBO dropped by 4.7%, to RUB 50.9 billion, which still represents the second highest box office result recorded in recent years. For the second year in a row Russia turned out to be the largest European market in terms of admissions, just ahead of France. In Turkey, GBO revenues rose by 3.0% to TRY 896.9 million, marking a new record high in spite of a slight decline in cinema attendance (-1.1%), due to an increase in the average ticket price.

Superhero franchise Avengers: Infinity Wars led the EU box office charts in 2018

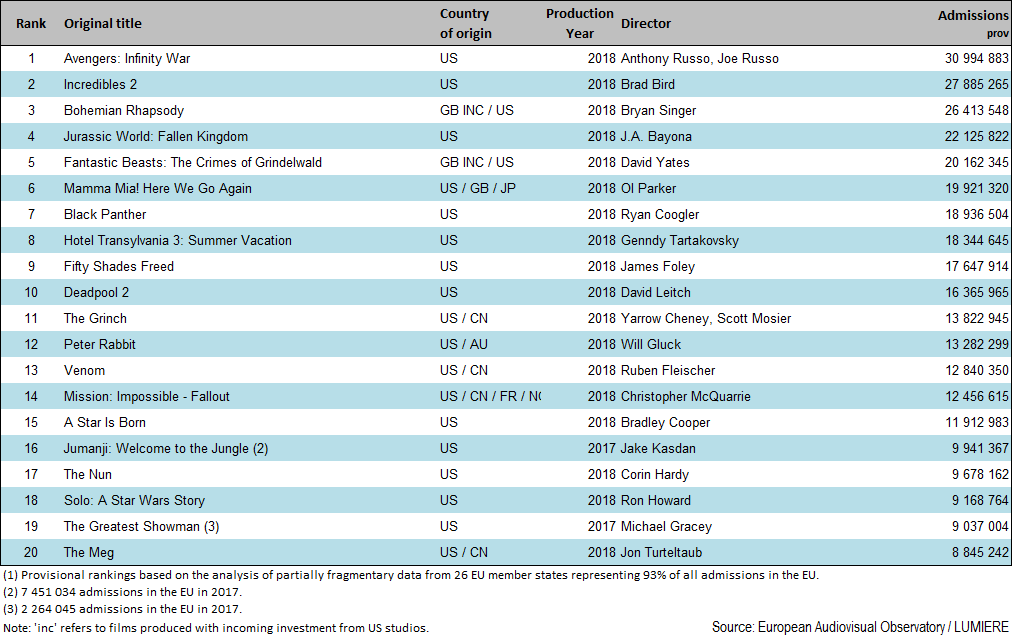

Once again, in 2018 US studio titles took the EU box office charts by storm, accounting for 18 out of the top 20 titles. Superhero blockbuster Avengers: Infinity Wars was the box office winner in 2018, the only title to generate more than 30 million admissions (31.0 million), followed by family animation feature Incredibles 2 (27.9 million). Other successful titles include Jurassic World: Fallen Kingdom (22.1 million), Mamma Mia! Here We Go Again (19.9 million), Black Panther (18.9 million) and Fifty Shades Freed (17.6 million). In line with previous years, 2018 saw a high prevalence of film franchises, with as many as 17 titles out of the top 20 (and 9 titles out of the top 10) being sequels, prequels, spin-off or reboots. In turn, only four films in the top 20 were family animation features, compared to six in 2017 and eight in 2016.

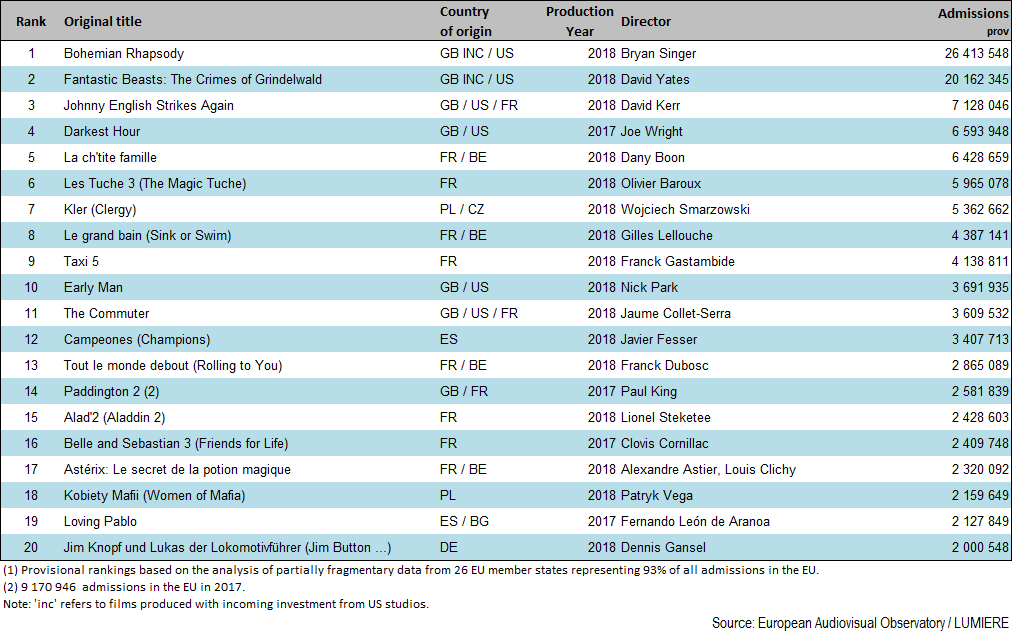

GB inc productions Bohemian Rhapsody and Fantastic Beasts: The Crimes of Grindelwald were the only two non US films to feature among the top 20 titles, generating 26.4 and 20.2 million admissions respectively. Leaving aside films produced with incoming US studio investment (EUR inc), Johnny English Strikes Again was the top European title for the year with 7.1 million admissions, followed by The Darkest Hour (6.6 million).

Table 1: GBO, admissions and national market share in European countries 2017 – 2018 prov

Table 2: Top 20 films by admissions in the European Union in 2018 prov (1)

Table 3: Top 20 European films by admissions in the European Union in 2018 (incl. “EUR inc”) prov (1)

European market share rose to 29.4%

In 2018 the EU decline in cinema attendance was mainly driven by a drop in admissions to US films leading to an estimated US market share of 63.2%, down from 66.2% in the previous year. In turn, the market share captured by European films grew from 27.9% to 29.4%. This is the second highest level in the past five years. On a national level, local European films performed particularly well in the United Kingdom (44.8%), France (39.5%), Poland (33.3%) and Denmark (29.8%). Outside the EU, Turkey was the European territory with highest national market share (63.4%).

Spurred by the performance of two GB inc productions among the top 20 films, the market share of films produced with incoming US investment (EUR inc) increased from 4.2% to 5.4%.

Table 4: EU market share by country of origin 2014 – 2018 prov

In % of total admissions. Provisional estimates.

EU film production volume increased again

After slowing down in 2017 for the first time, EU production levels rose again last year as the estimated number of European feature films produced in 2018 increased from 1 737 to 1 847. This figure breaks down into an estimated number of 1 142 fiction films (62%) and 705 feature documentaries (38%). The rise in production activity was primarily caused by an increase in the number of international co-productions and feature documentaries.

Table 5: Number of feature films produced in the European Union 2014 – 2018 prov

Provisional estimates.

EU screens infrastructure close to full digitisation

According to figures provided by MEDIA Salles the digitisation process in the EU is almost complete. By the end of 2018 a total of 24 EU member states had converted 90% or more of their screen base with only two territories registering digital screen penetration rates below 80%: the Slovak Republic (75%) and the Czech Republic (51%)[1]. By the end of 2018 the total number of digital screens was 31 246, accounting for an estimated 97% of the EU’s total screen base.

Table 6: Digital screens in the European Union 2014 – 2018 prov

Provisional estimates.

[1] Czech screen base includes non-permanent screens (open-air, part-time, itinerant screens) which represent an important part of the local cinema landscape. Digital screen penetration among permanent cinemas is above 90%.

More detailed information on European as well as international theatrical markets can be found in FOCUS 2019 World Film Market Trends prepared by the European Audiovisual Observatory for the Cannes Film Market. All film journalists receive a free press copy of FOCUS which can be picked up on the Observatory’s stand in the Palais des Festivals: Ground floor level 0, Riviera section, stand H3. Tel.: 33 (0) 4 92 99 32 18. Or contact: Alison Hindhaugh (Press Officer) [email protected] - tel.: +33 (0) 684352743. Focus 2019 will also be available to purchase on the stand, or via our website from 14th May. (see: http://shop.obs.coe.int/en/19-focus)

Notes for Editors:

- Data have been collected with the collaboration of the EFARN (European Film Agency Research Network).

- All 2018 figures are provisional.

The pan-European film rankings shown in tables 2 and 3 are based on data from all European Union countries for which results have been stored in the LUMIERE database as of 22nd April 2019. This database on admissions to films released in Europe is available online and free-of-charge, and is the result of collaboration between the European Audiovisual Observatory and various specialised national sources as well as the MEDIA Programme of the European Union. LUMIERE provides country-by-country admission data for about 49 000 films in distribution in Europe since 1996. Partial 2018 data for 33 European countries as well as the North American market is now available.

Market shares (Table 4)

The market shares shown in this figure are based on an analysis of results of films released in member states of the European Union for which admissions data for individual films are made available to the European Audiovisual Observatory. In order to draw up such market shares, a single 'country of origin' must be attributed to each film, an attribution that can prove difficult in the case of international productions. In these cases the Observatory's aim is to attribute a country of origin corresponding to the source of the majority financial input and/or creative control of the project. Since 2005 the Observatory has identified specifically films that have been produced in one or more European countries (or elsewhere) with US investment by using the reference 'inc' (incoming investment) in the country of origin attribution. It should be noted, however, that the availability of further information may occasionally lead to changes in the attribution of country of origin and that the origin of a film as attributed in the LUMIERE database may not always be identical with that indicated by national sources.

The provisional data on market shares in the European Union in 2018 shown in table 4 are based on the data on admissions to individual films as collected in the LUMIERE database on 22nd April 2019. At this date the coverage rate of the database for admissions in the 26 European Union countries for which data is available was of around 93%. Due to various gaps in data collection and delivery in various countries, coverage of 100% of admissions is currently unachievable.

Number of feature films produced in the European Union (Table 5)

Estimating the total volume of production of feature films in the European Union remains difficult, chiefly due to the risk of double counting of co-productions and to differing national methodologies for the collection of this data. Included in the total for the European Union are feature-length films intended for theatrical exploitation, excluding minority co-productions and US and foreign production in the United Kingdom. For some countries no separate data are available for feature fiction and feature documentary films.