Download "Insights into direct public film funding in Europe – A sample analysis of national and sub-national funds for the years 2018-2022" here

The European Audiovisual Observatory has just published a new report on direct public film funding in Europe. The purpose of this report is to provide high-level insights into the development of European film agencies’ income and activity spend between 2018 and 2022. Insights are generated based on data samples of national and sub-national film funds. Please refer to the report for methodological remarks and caveats.

A few key insights

1. National funds’ income and activity spend increased between 2018 and 2022, but less than the inflation rate

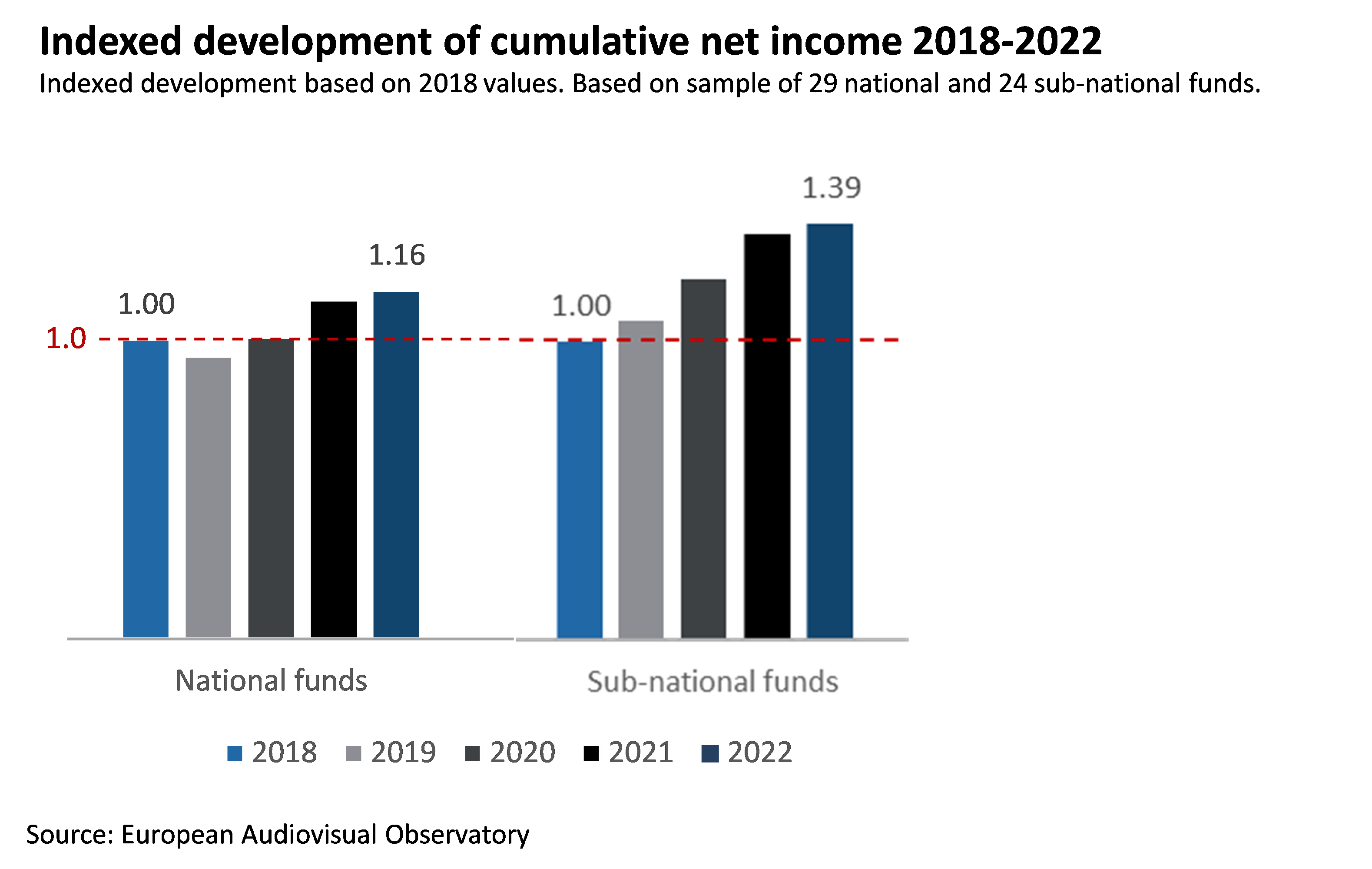

Funds’ income and activity spend increased strongly in 2020 and 2021, assumedly linked to COVID crisis support, but growth rates dropped sharply in 2022. The net income of national and sub-national funds in 2022 was 16% (for national) and 39% (for sub-national) higher than in 2018, respectively, and net activity spend was 8% (national funds) and 44% (sub-national funds) higher. This compares to an inflation rate of around 22% between 2018 and 2023 according to Eurostat.

2. There is no standard financing model for European film funds, but the vast majority of funds relied primarily and increasingly on government financing

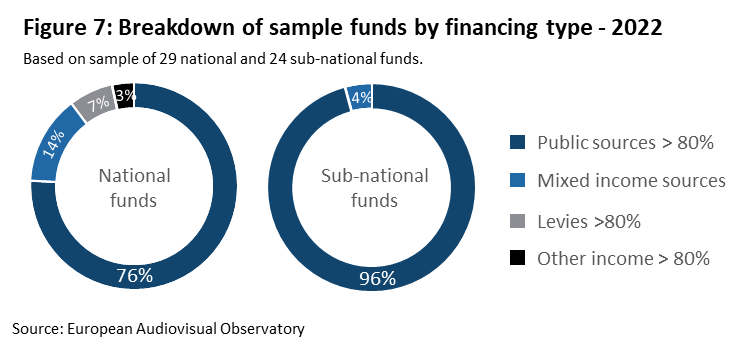

Fund income can be financed from a variety of sources and there are a number of different financing models across Europe. While a few national funds generate their income from up to eight different income sources, the vast majority of the sample funds relied on only one or two income sources. In the majority of cases this would be either state or regional government budgets combined with their own income. 22 out of the 29 national film funds in the data sample sourced more than 80% of their 2022 income from government budgets, while industry levies accounted for more than 80% of financing for two funds and only four funds had a more diverse financing mix.

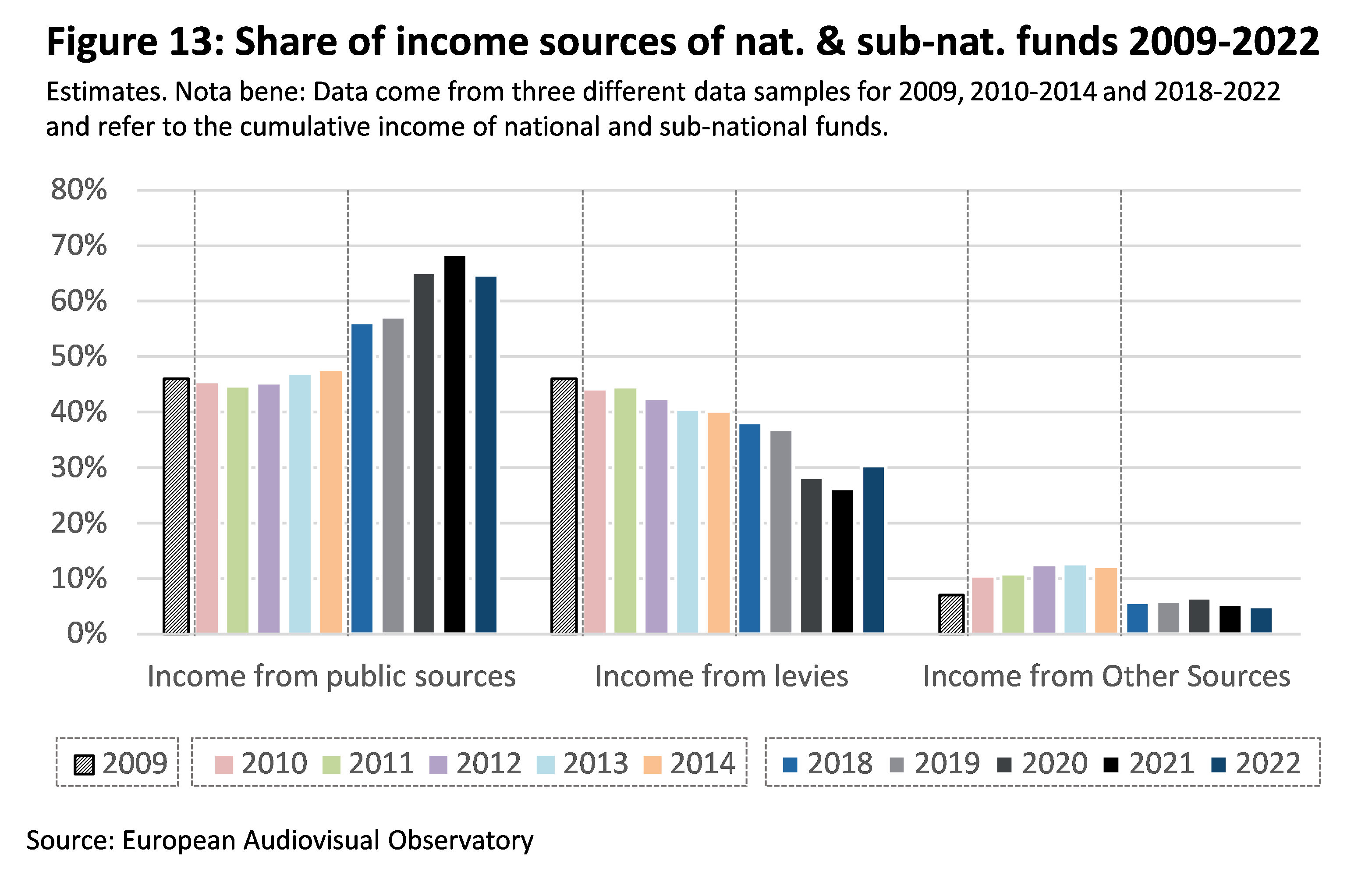

Over the past years, the role of industry levies on a pan-European level has been decreasing, while national funding has become more reliant on public sources as the percentage share of industry levies in the financing mix of national funds decreased from 40% in 2018 to 32% in 2022.

However, this drop in the financing share does not stem from a decline in the amount of actual levies, which in fact were 6% higher in 2022 than in 2018. Rather it is caused by a disproportionate growth in funds’ income which has been driven by increasing funds from public sources, whose financing share jumped from 54% in 2018 to 63% in 2022.

Although it is not possible to identify which part of the reported income is dedicated to incentives, it is likely that the strong increase in income from public sources is driven by the increase in budgets dedicated to incentives as well as COVID related public support in 2020 and 2021. The effect of the implementation of investment obligations which could lead to an increase in the financing share of levies may only become visible from 2023 onwards.

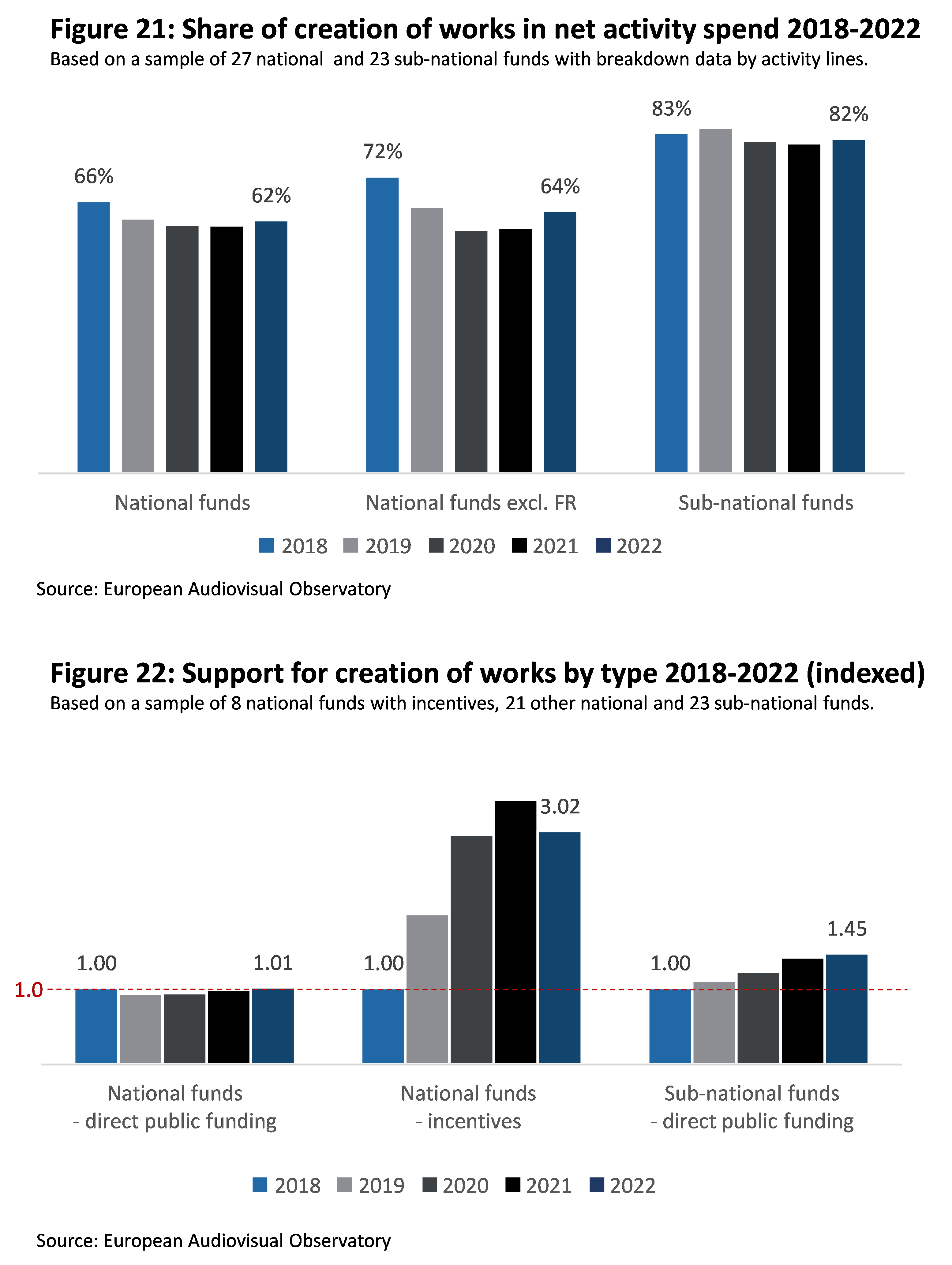

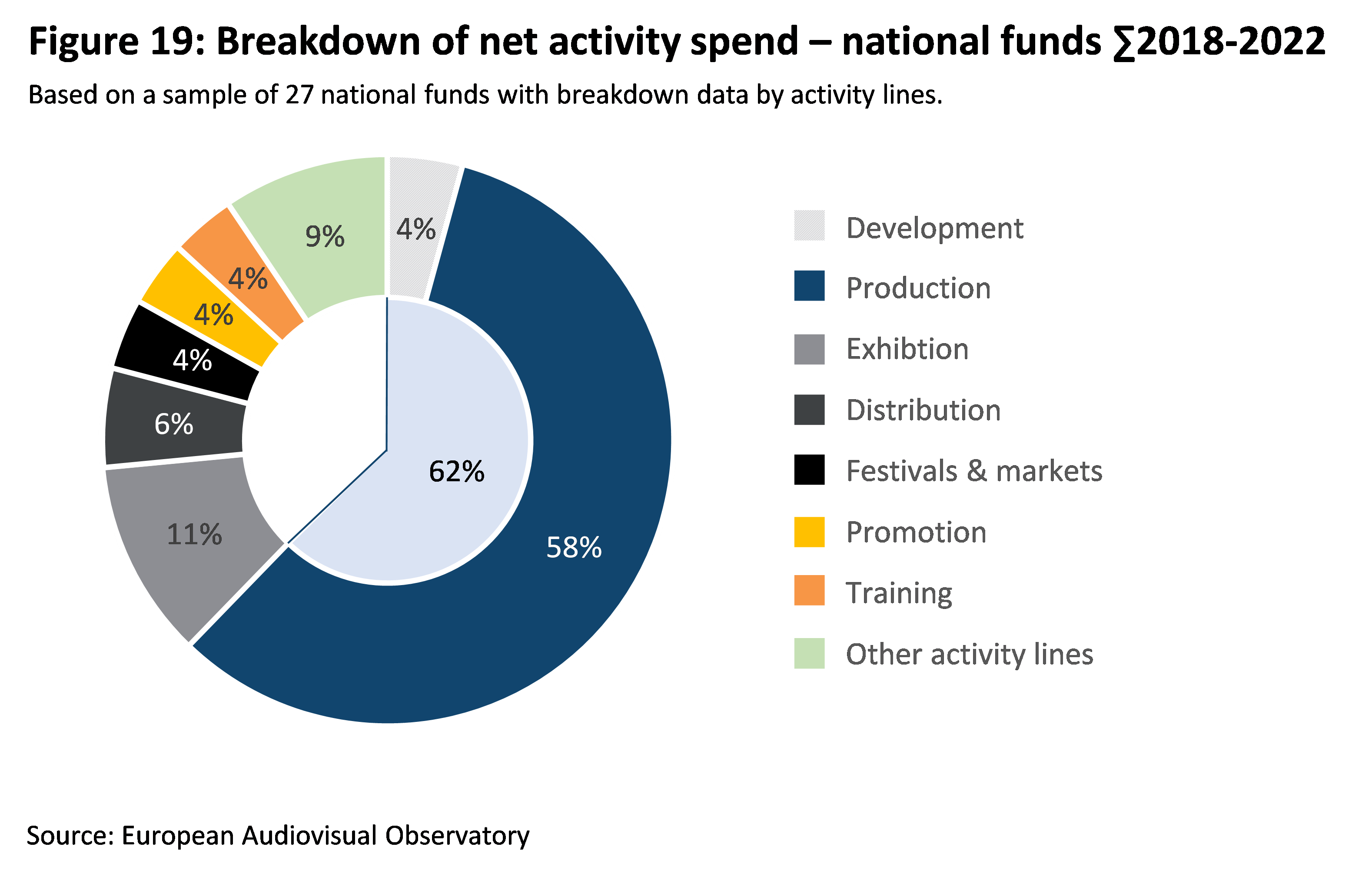

3. While the lion’s share of direct public funding goes to the creation of works, its percentage share decreases as production support grows in the form of incentives

In line with the initial core purpose of most film funds, the majority of their funding has traditionally been allocated to supporting the creation of works and the period 2018 to 2022 is no exception. In the case of national funds, 62% of their direct public funding spend went to the production (58%) and development (4%) of film and other audiovisual works. In the case of sub-national funds, which generally have a narrower mandate compared to national funds, the share of support for the creation of works was significantly higher, namely 82% of their cumulative net activity spend (73% to production, 8% to development).

However, the share of direct public funding support provided by national funds for the creation of works declined from 66% in 2018 to 62% in 2022. The declining share can be explained by the increase in direct public funding going to other activity lines rather than a decline in direct public funding of the creation of works in absolute terms, which has been stable over the time period covered. At the same time, the amounts of incentive support dedicated to the development and production of films and audiovisual works provided by eight national sample funds have tripled over these five years.