|

The figures in this press release are taken from the 2026 edition of FOCUS – World Film Market Trends, a report which is prepared each year for the Marché du Film. Journalists may request a PDF press copy from [email protected]. FOCUS is available as a free print copy to all Marché attendees from the Observatory’s stand (H1 in the Riviera/Marina section) It’s also free online for all Marché participants on the online platform. It can be purchased after the Marché from Council of Europe bookshop.

Click here for our table of detailed GBO, admissions and national market shares in Europe

Asia drives global box office growth, while cinema attendance declines in Europe by 5%

An estimated 4.98 billion cinema tickets were sold in the 82 markets covered in its FOCUS publication. This marked a 3% increase compared to 2024 driven primarily by rising cinema attendance in Asia (+10%), notably in China and Japan, while admissions declined in Europe (-5%) and Latin America (-8%). Estimated global GBO increased by 5% in 2025 to EUR 29.56 billion, indicating that global box office figures in 2025 continued to remain approximately 30% below the pre-pandemic average. Cinema-going was heavily concentrated among the world’s leading markets, with the 10 largest markets cumulatively accounting for 77% of worldwide admissions and 76% of GBO.

US films continued to dominate the box office in most countries except for Asian markets, where national films lead the market. This was most notable in India (national market share of 90%), Japan (76%) and China (74%). Accounting for 36 of the top 50 films worldwide US films cumulatively captured an estimated 52% of global admissions compared to 63% in 2019. Conversely, the market share of Asian films increased from 27% in 2019 to 36% in 2025, with a Chinese film, Ne Zha 2 (CN), becoming the first non-US studio film to top the world charts by reaching a GBO of almost EUR 1.8 bn. (Note: This figure is changed on 12 May 2026. Original text was "Conversely, the market share of Asian films increased from 27% in 2019 to 36% in 2025, with a Chinese film, Ne Zha 2 (CN), becoming the first non-US studio film to top the world charts by reaching a GBO of almost almost 1.8 billion tickets sold")

Cinema attendance in Europe down due to comparatively poor performance of US films and lack of French blockbusters

Admissions in Europe decreased by 5% to 795 million, mostly due to decline on the French market in 2025 and an overall comparatively weak performance of US films. While US studio films continued to dominate the European top charts, accounting for 18 of the top 20 films, only 12 of them sold over 10 million tickets, compared to 20 films before the pandemic. Franchises dominated the charts, representing 16 of the top 20 films. Minecraft (US), the live-action adaptation of the video game of the same name, topped the charts in 2025 with 29 million admissions, significantly less than 2024’s top film Inside Out 2 (US) which sold 51 million tickets. Following Minecraft were Lilo & Stitch (US) (28 million admissions) and Zootopia 2 (US) (27 million admissions). As a late 2025 release, the latter continued to be screened in 2026, alongside Avatar: Fire and Ash (US) which ranked 4th in 2025.

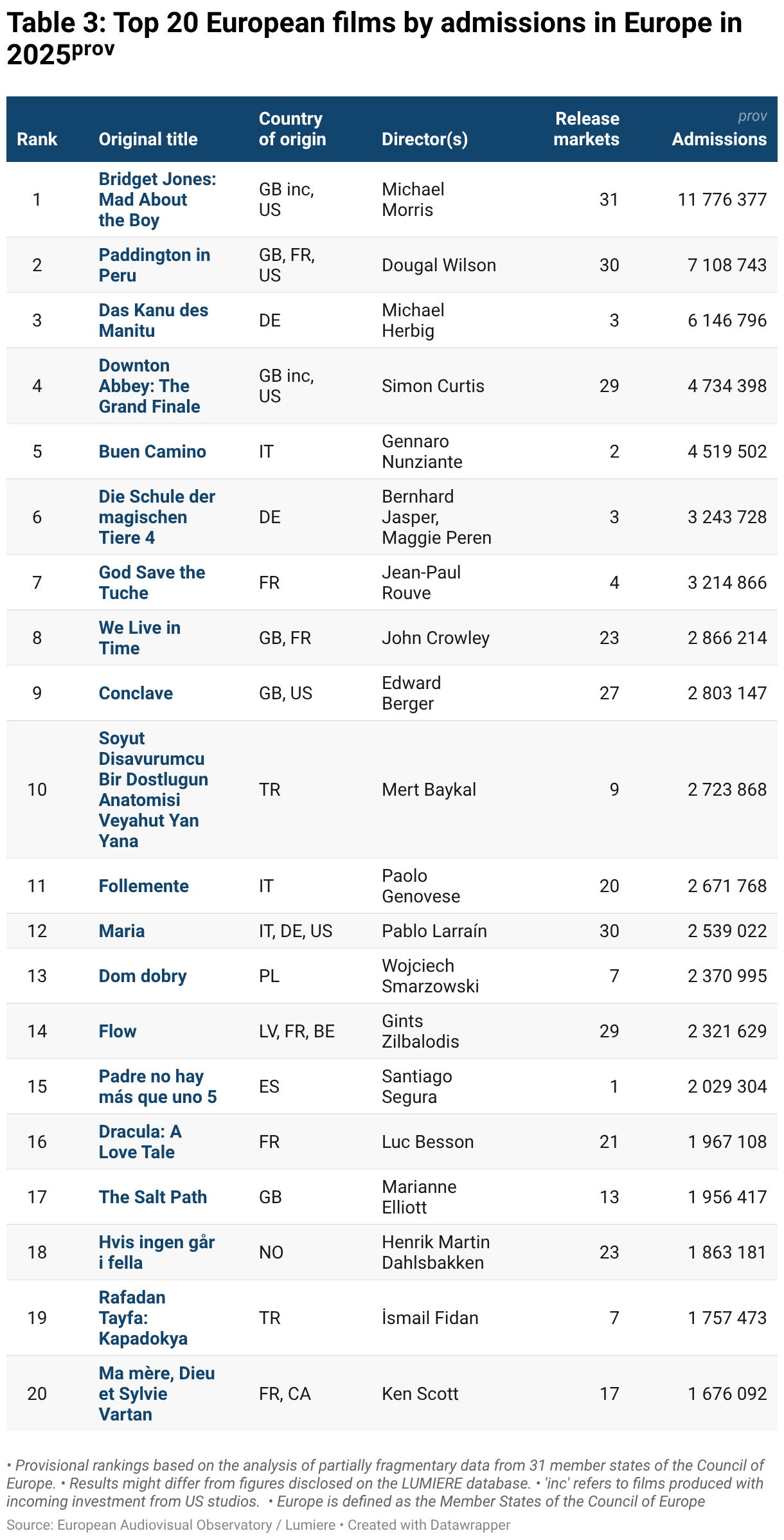

The top 20 European films in 2025 displayed an unusual diversity in nationality, challenging the traditional dominance of French and British titles. Ten were local breakout films (where over 80% of admissions occurred in their home markets), and eight generated most admissions outside their country of origin. Among these were Paddington in Peru (GB), Maria (IT), and Flow (LV).

A total of 112 films exceeded the 1 million admissions thresholds, including 41 European films, consistent with 2024 but well below pe-pandemic levels when 155 films exceeded 1 million admissions (including 63 European titles). Collectively, the 20 highest-performing films generated 278 million admissions, accounting for 35% of Europe’s total admissions.

Continued strong market share for European films

Capturing an estimated 31.4% of total admissions, the market share of European films remained well above the pre-pandemic average of 28%, despite declining by 2 percentage points compared to 2024. Meanwhile, US films’ market share remained at a comparatively low level of 62%. Türkiye maintained its position as the European leader in terms of national market share at 54.8%, followed by France (37.9%). The United Kingdom ranked next with 40.5% when including inward investment films such as Bridget Jones: Mad About the Boy, which accounted for 33.7%, while UK independent productions accounted for only 6.8% of total admission in the UK. Denmark (37.3%), Italy (33.3%), Albania (32.0%), and Norway (31.3%) also achieved market shares above 30%.

In 14 European countries, a European film ranked first among the Top 10, and in 12 of these countries, it was a national production, including in Germany and Italy. In Denmark, an exceptional six national films were among the Top 10 in 2025. In Austria and Cyprus, the top-ranking films were a German and a Greek production, respectively.

Spain drives ongoing growth in European production volume

European film production continued to crawl to yet another record high in 2025, with 2 522 films produced across Europe, 20 more than in 2024 and 297 more than the pre-pandemic average. This total included 1 504 fiction films (-51 compared to 2024) and 1 018 documentaries (+71 compared to 2024).

Most of the production increase at pan-European level originated from Spain, which produced 99 films more than in 2024. Poland followed (+26 films), then Denmark (+11 films), and Austria (+11 films). This growth was offset by declining production volumes in other countries, most notably Türkiye (-64 films), Switzerland (-26 films), the Netherlands (-22 films), and Greece (-21 films).

Thanks to its production surge, Spain became Europe’s leading film producer in 2025 with 423 films, with Italy ranking second (357 films). The United Kingdom, France, and Germany followed, with 282, 228, and 178 films produced respectively.