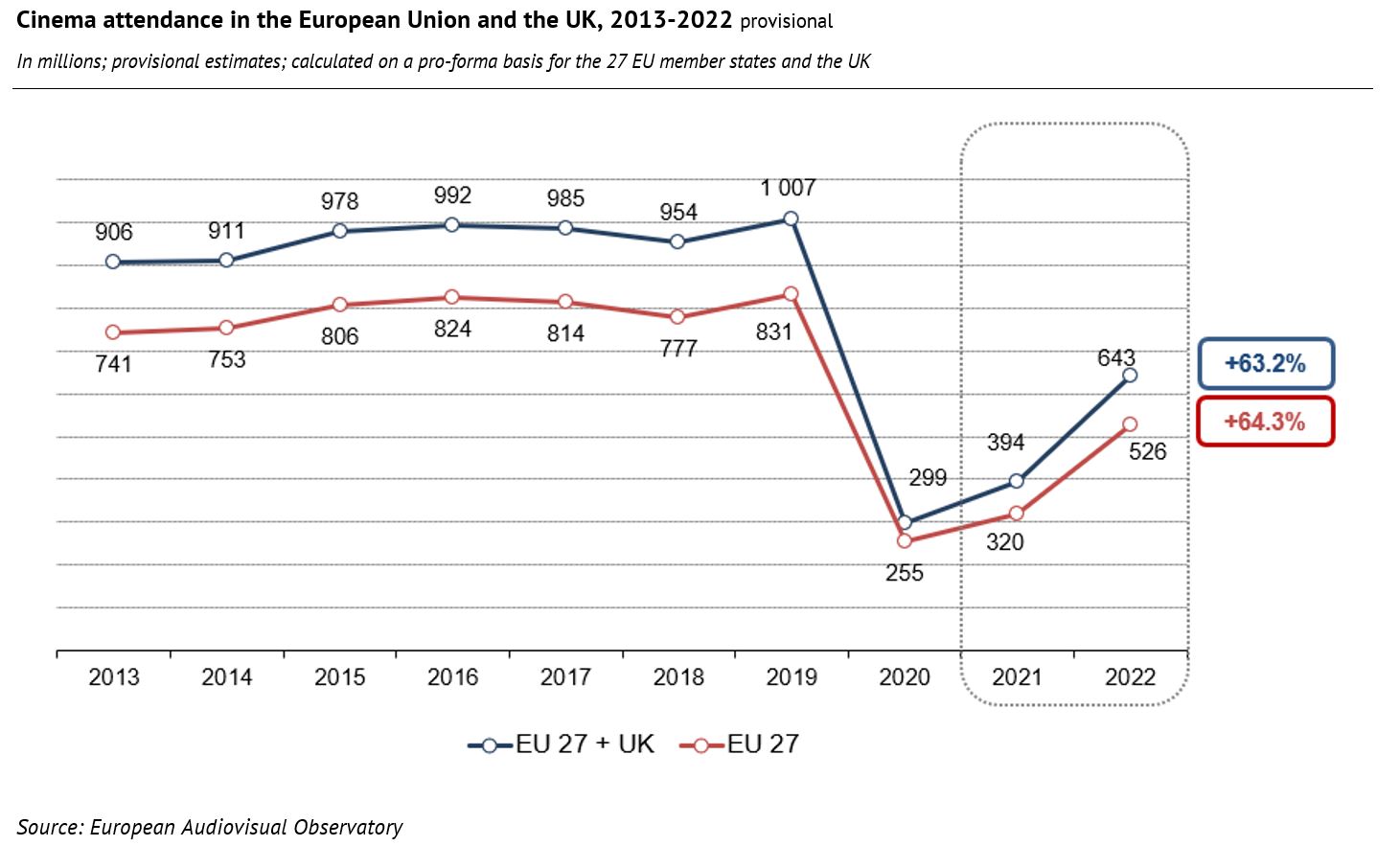

Based on preliminary data collected by the European Audiovisual Observatory, cinema attendance in the European Union and the United Kingdom reached an estimated 643.0 million admissions in 2022. This corresponds to a year-on-year increase of 63%, and 249.0 million tickets more than in 2021. A similar rebound was observed when considering the European Union only (EU27), where ticket sales hit an estimated 525.8 million in 2022, 205.7 million admissions more than in 2021, +64% year-on-year.

While these preliminary results represent a clear improvement compared to 2021 (when cinemas were shut down intermittently in several markets), they still fall significantly short of pre-pandemic levels. In the EU and the UK, ticket sales for 2022 were 34.5% below the 2017-2019 average, accounting for an estimated loss of 338.9 million tickets. A similar decline compared to the pre-pandemic average (-34.9%, -281.7 million admissions) was observed for the European Union only (EU27). The figures show that the European theatrical sector has not fully recovered from the crisis in 2022, amid audience hesitancy and other side effects of the pandemic.

Cinema attendance in the European Union and the UK, 2013-2022 - provisional

In millions; provisional estimates; calculated on a pro-forma basis for the 27 EU member states and the UK

![]()

Source: European Audiovisual Observatory

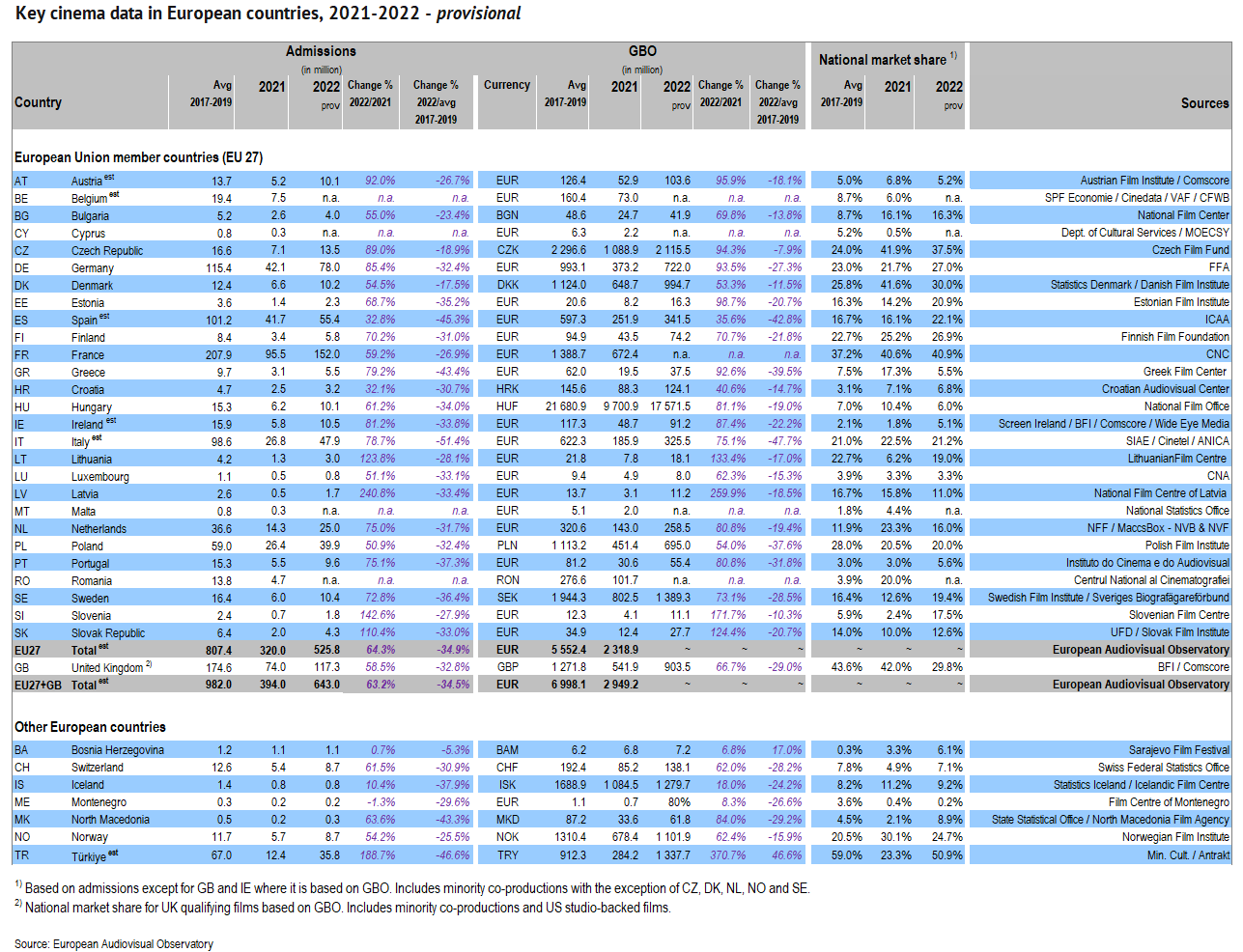

Overall admissions for 2022 grew in the large majority of territories for which data were available, with significant differences across individual countries. However, in all markets analysed, ticket sales failed to match the numbers registered before the COVID outbreak. In the EU, the year-on-year increase in attendance was significantly above average in Latvia (+241%, + 1.2 million admissions), Slovenia (+143%, +1.0 million), Lithuania (+124%, +1.7 million), the Slovak Republic (+110%, +2.2 million) and Germany (+85%, +35.9 million). Conversely, interannual growth was comparatively low in Poland (+51%, + 13.4 million admissions), Spain (+33%, +13.7 million) and Croatia (+32%, +0.8 million). France recorded the largest admission volume in Europe for 2022, with a total of 152.0 million tickets sold (+59% on 2021).

Denmark was the EU country showing the highest degree of recovery against pre-pandemic attendance levels, as admissions made up as much as 82% of the 2017-2019 average. A relatively strong recovery was also observed in the Czech Republic where admissions for 2022 represented 81% of the pre-pandemic average, Bulgaria (77%), Austria and France (73%). On the other hand, recovery was more limited in Italy where only 47.9 million tickets were sold in 2022, representing less than half of the average attendance levels between 2017 and 2019.

Outside of the EU, ticket sales went by up 58% in the UK, to 117.3 million admissions, 43.3 million more than in 2021 and corresponding to 67% of pre-pandemic levels. In Türkiye, ticket sales jumped to an estimated 35.8 million admissions in 2022, a whopping 189% increase on 2021, but only accounting for 53% of the 2017-2019 average.

While it is too early to analyse admissions by origin, preliminary data suggest that in the EU and the UK the box office was mainly driven by the success of US studio hits, including Avatar: The Way of Water (US), Top Gun: Maverick (US) and Minions: The Rise of Gru (US).

Compared to 2021, the market share captured by domestic films increased in half of the 24 EU markets for which 2022 data were available, rising above the 2017-2019 average in 16 territories. France registered the highest market share for national productions in the EU (41%), ahead of the Czech Republic (37%), Denmark (30%), Finland and Germany (27%). Outside of the EU, the market share for national films decreased to 30% in the UK (including US studio-backed productions), which compares to 42% in 2021 and an average 44% between 2017 and 2019. Independent UK productions only captured 8% of GBO takings, up from 6% in 2021 and compared to a pre-pandemic average of 12%. Türkiye saw the domestic share rising from a record low of 23% in 2021 to 51% in 2022, slightly below the levels registered in previous years.

Key cinema data in European countries, 2021-2022 - provisional

![]()

![]()

1) Based on admissions except for GB and IE where it is based on GBO. Includes minority co-productions with the exception of CZ, DK, NL, NO and SE.

2) National market share for UK qualifying films based on GBO. Includes minority co-productions and US studio-backed films.

Source: European Audiovisual Observatory

Link to this data in the form of an Excel table.

Notes:

- Data have been collected with the collaboration of the EFARN (European Film Agency Research Network).

- All 2022 figures are provisional.

Our next cinema figures will be released just before the Cannes International Film Market.

To be added to our press listings, send an email to: [email protected]